Background

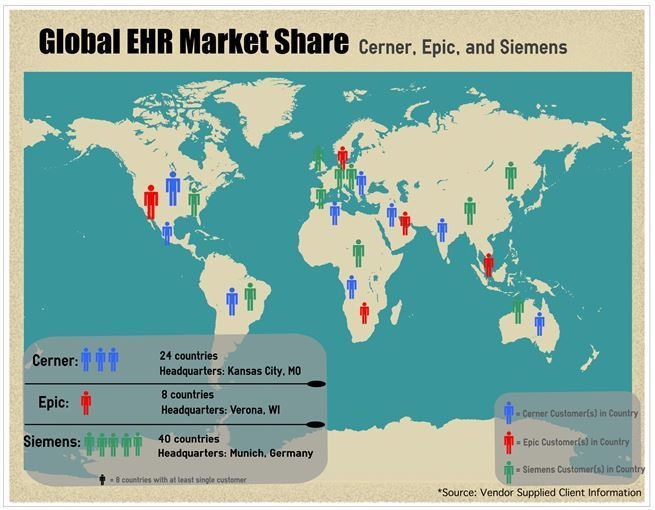

On August 5, Cerner Corporation announced the acquisition of Siemens AG’s Healthcare Information Technology business unit for $1.3 billion. This will result in an organization with 20,000 employees spanning more than 30 countries and 18,000 client facilities, with an R&D budget of $650 million and combined annual revenues of $4.5 billion. The two companies also formed a strategic global alliance focused on increasing the integration capabilities between Cerner’s EHR and Siemens’ medical devices. With a preliminary 3-year term and $50 million investment from each organization, the integration effort will initially focus on laboratory automation and cardiology information systems. Customers and their previously independent vendors must now determine how this acquisition will impact the combined software road map, vendor services, and overall strategic vision.

Implications for Customers

During its investor announcement Webcast, Cerner committed to supporting existing Siemens customers for at least the next decade. Early indications, however, are that Cerner will focus on adoption of the Cerner Millennium platform across its newly expanded and future customer base. Per Marc Naughton, Cerner Executive Vice President and CFO, “What we’re doing here is clearly not for solutions or for their intellectual property relative to their existing platforms. We are still committed to Millennium. It is our go-forward platform, and it will continue to be so.” Current Siemens customers should expect Cerner to aggressively attempt to transition them to Millennium over the next 10 years via a new “rapid migration tool” that Cerner hopes can help combat customer attrition. John Glaser, CEO of Siemens Health Services, indicated that Siemens clients will have to weigh “not just features and functions but technical support and services and cost … I think they [Siemens clients] are waiting, and we’ll have some more answers for them by the end of the calendar year.”

From a product road map perspective, current Cerner customers should feel confident that their existing products will only improve. Siemens’ Soarian financial applications have historically been stronger in functionality than those of Cerner. However, Cerner has made major investments in its financial systems in recent years, and ongoing investment and development are not expected to decline. The addition of Soarian R&D expertise will augment existing Cerner resources and should help reinforce Cerner’s focus on improving population health and care coordination.

For prospective customers, there may be concerns about vendor services as Cerner attempts to support ongoing and contracted implementations of both its and Siemens’ existing clients. Cerner also recently bid for the U.S. Department of Defense EHR contract with Leidos and Accenture, which, if successful, could further strain its implementation resources. On the flip side, the strategic global alliance has the potential to improve the EHR device integration, which could help cement Cerner’s desire to be the most interoperable EHR vendor in the market. Prospective clients should pay particular attention to whether Cerner’s and Siemens’ industry rankings can be maintained in the next few years or if growth, leadership team alignment efforts, and a broader overall suite of products result in a decline in functionality and/or support services.

Implications for Other Vendors

The Siemens acquisition serves as a way for Cerner to expand its existing hospital base, as well as acquire a large international footprint. These should both be considered a direct challenge to Cerner’s main competitor, Epic Systems Corporation. Also, it is expected that Cerner will pursue a strategy of substantial price discounts to dissuade the existing Siemens customer base from considering a move to comparably expensive Epic products. Given that the majority of Siemens’ customers are hospitals with less than 200 beds, Cerner may be trying to expand to a demographic that Epic has not historically pursued (although Epic’s recent push for Community Connect and regional integration targets smaller markets). Only time will tell if Cerner will be able to avoid some of the difficulties that Allscripts experienced after its acquisitions of Misys and Eclipsys or the integration struggles that acquisition-hungry companies like GE Health and McKesson Corporation have had in recent years.

More to Come

This is the first in a series of posts that will outline key considerations for established and prospective Cerner customers, as well as established Siemens customers.